It has been 10 years since the great financial crisis and its aftermath which led us into an environment that has been characterised by change, change, and more regulatory change. During that time, risk and compliance officers have risen to the task of managing the continuing challenges, as cited in the annual Thomson Reuters Regulatory Intelligence (TRRI) Cost of Compliance 2019 report.

The Cost of Compliance 2019 report has become the trusted voice for risk and compliance practitioners around the world. Over the lifetime of the report, there have been almost 6,000 participants and more than 40,000 downloads of the report by financial services firms, global systemically important financial institutions (G-SIFIs), regulators, law firms, domestic governments, and consultancies.

The unparalleled interaction with the global financial services industry and the frank and wide-ranging concerns shared by practitioners continues to bring unique insight into the practical reality and challenges faced globally by risk and compliance officers.

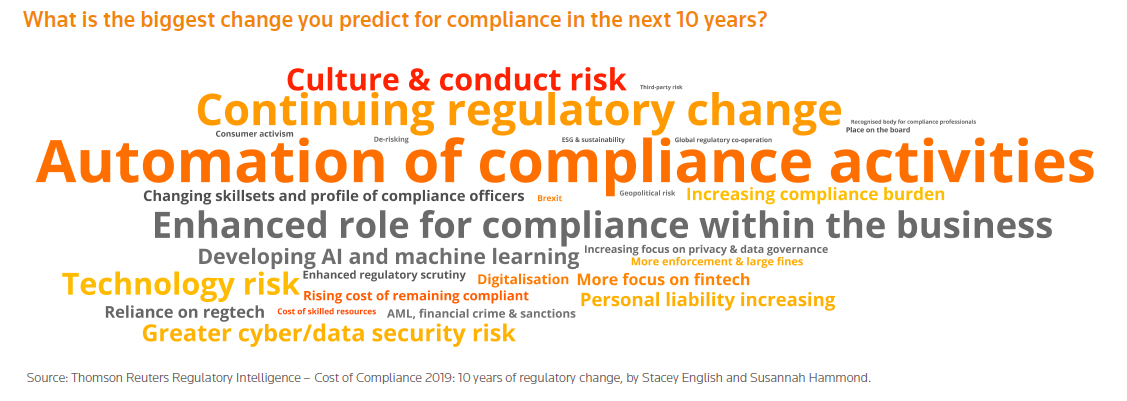

As the survey shows, compliance officers can continue to expect to face complex challenges in the year ahead with regulatory change identified as the single biggest concern. For 2019, the most commonly cited challenges included: increasing regulatory burden; financial crime, anti-money laundering and sanctions compliance; culture and conduct risk; and the adequacy and availability of skilled resources.

Broadly in line with compliance expectations, the biggest challenges facing boards of directors in the coming year include keeping up with regulatory change; cyber-resilience; personal accountability; and, culture and conduct risk.

Focus on Risk

Since the financial crisis, financial services firms have seen unprecedented levels of regulatory change as governments and policymakers have sought to ensure that a similar global downturn could not happen again.

Ten years ago, there was an understandable focus on financial stability, and, in policy terms, that led to the creation of the Financial Stability Board (FSB), a supranational body that sets the policy direction for financial services firms around the world. It is to the FSB that risk and compliance officers now look to as the original source for much of the regulatory change continuing to be introduced around the world.

There are three key areas where the role and expectations on the compliance function have dramatically changed over the last 10 years:

- Culture and conduct risk

- Personal liability

- Technology

The inclusion of culture and conduct risk in the stated regulatory expectations around the world has become the new normal with financial services investing heavily to tackle the how as well as the what with regards to substantive issues such as firm culture, sales practices and how best to consistently demonstrate the required good customer outcomes.

Over the last few years, culture and conduct risk issues are no longer being considered as a separate and distinct area of risk and compliance, but rather they have moved much closer to being seen as inherent in the business—and treated as such.

Check out the video interview with the authors of the report

Indeed, the capacity to be able to demonstrate a strong positive culture in action, as well as the ability to mitigate any conduct risks arising, has become a required core competency for firms and their compliance officers with all of the challenges associated with a qualitative, rather than a quantitative, issue.

On personal liability, there has been an inexorable rise in the implementation of accountability regimes around the world. Substantive regimes have been introduced in Australia, Hong Kong and the UK—with Ireland and Singapore in the planning or consultation stages. As with so many aspects of regulation, the compliance function may well take the lead in determining how best to identify, manage, and mitigate the rise of personal liability in financial services firms with the added complexity of having to accommodate evolving culture and conduct risk expectations.

While accountability regimes cover all senior individuals in a firm, compliance officers are continuing to expect an increase (60 percent in 2019) in their own personal liability.

Download your copy of the Thomson Reuters Regulatory Intelligence Cost of Compliance 2019 report.